Instant access through API, streaming or SFTP channel

Interest Rate Swap Volatility Indices

Model‑free implied volatility indices derived from swaption markets, capturing volatility across interest rate swaps in major currencies and tenors.

Model free swap volatility reference points

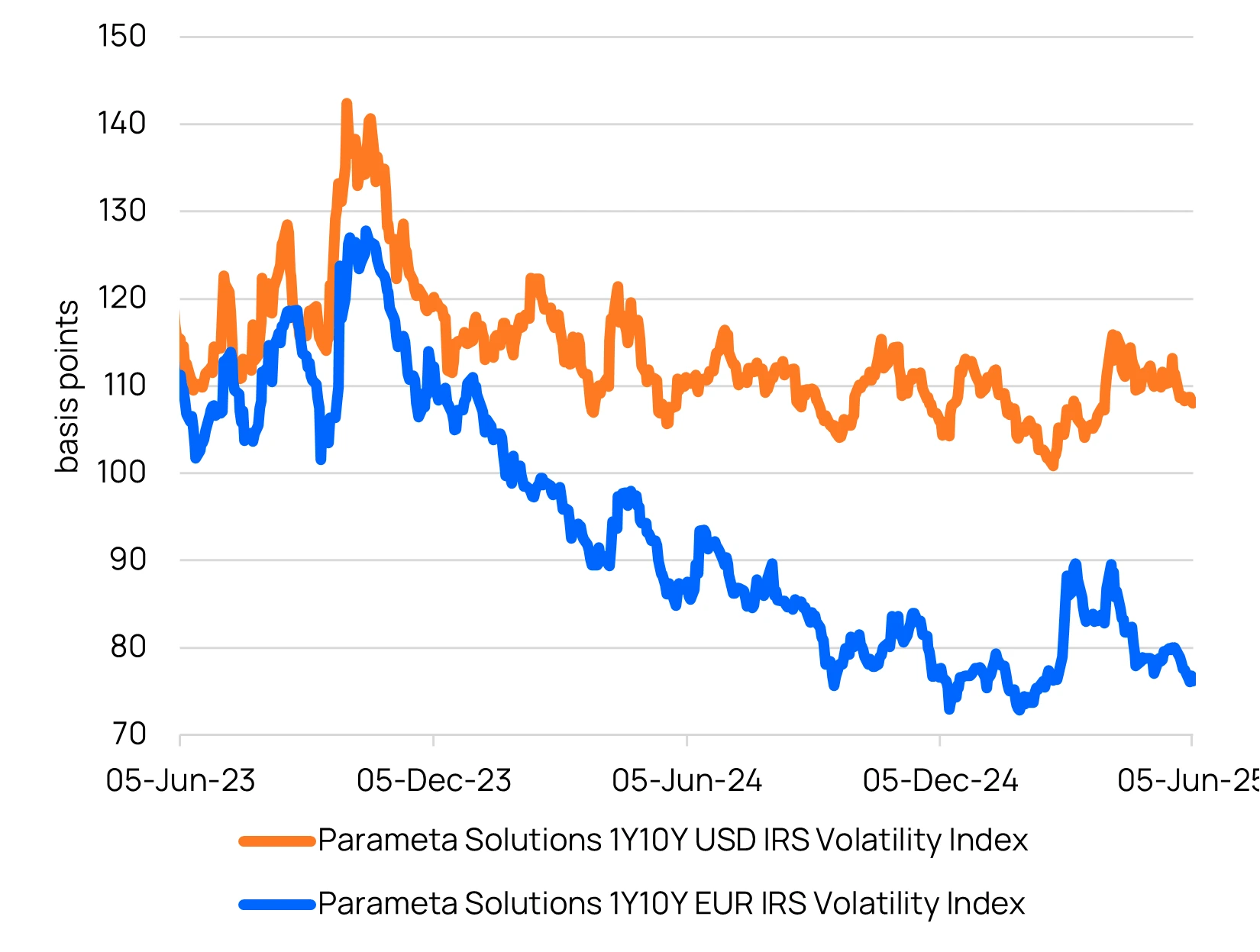

Parameta’s Interest Rate Swap Volatility (IRSV) Indices provide a model‑free measure of implied volatility across the USD, EUR, GBP, JPY, and AUD interest rate swap markets, covering the most liquid option expiry and swap tenor combinations.

Derived from swaption prices using tick‑level OTC data, each index captures the full information content of both at‑the‑money and out‑of‑the‑money strikes, delivering a more complete and forward‑looking view of market volatility.

Designed for real‑world application, the indices support volatility forecasting, risk management, and structured product strategies, with an aggregate index also available to provide a consolidated view of market‑wide swap volatility.

Chart Source: Parameta Solutions. All index data current as of 18/07/2025.

USD Interest Rate Swap Volatility Indices (USD IRSV)

Download FactsheetEUR Interest Rate Swap Volatility Indices (EUR IRSV)

Download FactsheetGBP Interest Rate Swap Volatility Indices (GBP IRSV)

Download FactsheetJPY Interest Rate Swap Volatility Indices (JPY IRSV)

Download FactsheetAUD Interest Rate Swap Volatility Indices (AUD IRSV)

Download FactsheetThree Easy ways to connect to our data

Direct

Cloud Delivery

Multiple solutions including AWS and Snowflake

Channel partners

Connect via Bloomberg

Request more info

Complete the form and tell us which asset class/instrument you would like to see.

FAQs on Interest Rate Swap Volatility Indices Data

What do Parameta’s swap volatility indices measure?

The Parameta Solutions Interest Rate Swap Volatility indices aim to provide market participants with a model-free measure of spot implied volatility in the interest rate swap markets. Derived from interest rate swaption prices, an index is available for each of the 48 most liquid option expiry, swap tenor combinations. Each index distils the information content of up to 24 different At-The-Money (ATM) and Out-Of-The-Money (OTM) payer and receiver strikes into a single measure of implied volatility for each option expiry/swap tenor combination.

Which markets do Parameta’s swap volatility indices cover?

Parameta offers swap volatility indices across key global markets, including USD, EUR, GBP, AUD, and JPY, enabling consistent volatility measurement across major interest rate environments.

How are the indices constructed?

Each index is derived from swaption pricing data, combining information from both at‑the‑money (ATM) and out‑of‑the‑money (OTM) payer and receiver options into a single implied volatility measure for each tenor/expiry combination.

The index calculation methodology is based on academic research* which provides a theoretical foundation for measuring interest rate swap volatility based on the model-free fair value of variance swap contracts for forward swap rates.

Each index is derived from the following inputs:

- Swaption ATM mid-price premium

- Swaption ATM normal volatility

- Swaption skew mid-price premia across the following payer and receiver strikes 1000, 500, 400, 300, 200, 150, 100, 75, 50, 25 and 12.5 for the specified option expiry and swap tenor.

*Source: Mele, Antonio & Obayashi, Yoshiki. (2015). The Price of Fixed Income Market Volatility. 10.1007/978-3-319-26523-0_3

What makes Parameta’s volatility indices different?

Unlike traditional volatility measures, Parameta’s indices use a model‑free methodology, which captures a broader set of option market information and is widely considered to provide more robust and forward‑looking volatility signals.

How can swap volatility indices be used?

These indices are used by market participants for:

- Volatility forecasting and trading strategies

- Portfolio risk management

- Derivatives pricing and structuring

- Benchmarking interest rate volatility across markets

They also support both single‑tenor analysis and aggregate market views through composite index measures.